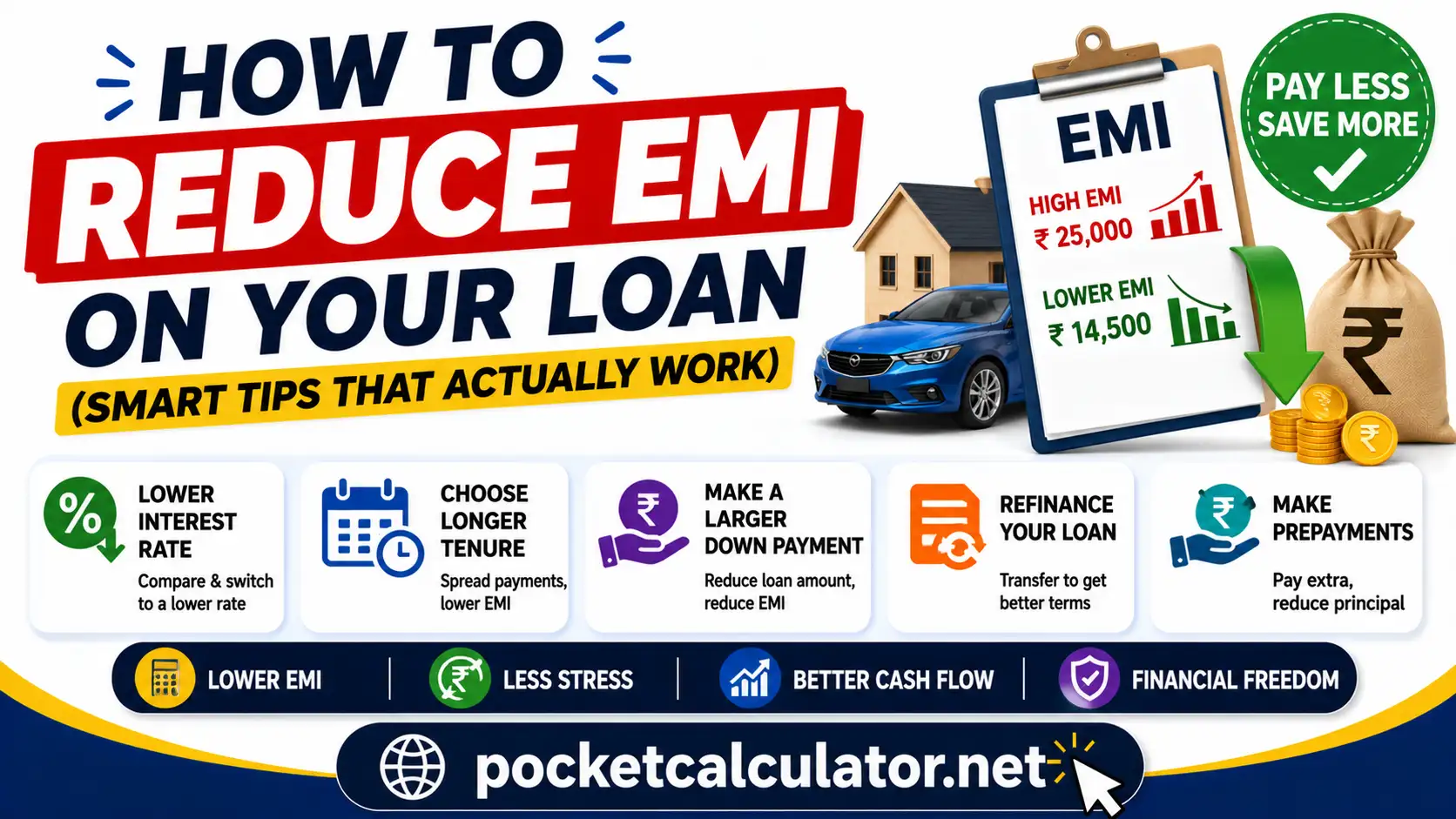

💸 How to Reduce EMI on Your Loan (Smart Tips That Actually Work)

Taking a loan can feel like a relief at first—whether it’s for a car, home, or personal need. But once the EMIs start hitting your bank account every month, reality kicks in.

You might find yourself thinking:

👉 “Can I reduce my EMI somehow?”

👉 “Is there a smarter way to manage this loan?”

The answer is yes. And not just one way—there are multiple practical, proven strategies that can help you reduce your EMI burden without hurting your financial stability.

Let’s walk through them step by step, in simple language, with real-life clarity.

🤔 First, What is EMI Really?

EMI (Equated Monthly Installment) is the fixed amount you pay every month toward repaying your loan. It includes:

- 💰 Principal (loan amount)

- 📈 Interest (charged by lender)

Your EMI depends on three main things:

- Loan amount

- Interest rate

- Loan tenure

👉 To reduce EMI, you need to adjust one or more of these.

🧠 Why Reducing EMI Matters

Lower EMI isn’t just about saving money—it’s about reducing stress.

- ✔️ More breathing room in your monthly budget

- ✔️ Better ability to handle emergencies

- ✔️ Less financial pressure

But here’s the truth:

👉 Reducing EMI the wrong way can increase your total cost

So the goal is not just lower EMI, but smarter EMI.

🔧 10 Smart Ways to Reduce Your EMI

Let’s explore practical strategies you can actually use.

1️⃣ Increase Your Loan Tenure (Quick Relief Option)

This is the easiest way to reduce EMI.

📉 How it works:

- Longer tenure → EMI reduces

- But → total interest increases

📊 Example

| Tenure | EMI | Total Interest |

|---|---|---|

| 5 years | ₹12,000 | ₹1.5 lakh |

| 7 years | ₹9,500 | ₹2.2 lakh |

👉 You save monthly, but pay more overall.

Best for:

Short-term financial pressure

2️⃣ Negotiate a Lower Interest Rate 📉

Most people don’t even try this—but you should.

💡 How to do it:

- Show good credit score

- Compare offers from other banks

- Ask your current lender for better rate

Even a 0.5% reduction can save thousands.

3️⃣ Make a Partial Prepayment 💰

If you have extra savings, use it wisely.

✔️ Benefits:

- Reduces principal

- EMI reduces OR tenure shortens

🧮 Example:

If you prepay ₹1 lakh on a ₹6 lakh loan:

- Your EMI may drop significantly

- Or your loan ends earlier

👉 Always check for prepayment charges.

4️⃣ Refinance Your Loan 🔄

This means shifting your loan to another lender offering better terms.

When it makes sense:

- Interest rates have dropped

- Your credit score has improved

⚠️ Watch out for:

- Processing fees

- Hidden charges

5️⃣ Choose Step-Down EMI Plan 📉

Some lenders offer flexible EMI structures.

📌 How it works:

- Higher EMI initially

- Lower EMI later

👉 Good for people expecting income changes (like nearing retirement)

6️⃣ Improve Your Credit Score 📊

Your credit score directly impacts your interest rate.

✔️ Tips:

- Pay EMIs on time

- Clear credit card dues

- Avoid too many loans

👉 A better score = better loan terms

7️⃣ Switch from Fixed to Floating Rate 🔁

If interest rates in the market are falling, switching can reduce EMI.

📌 Difference:

- Fixed rate = constant EMI

- Floating rate = changes with market

👉 Useful in a falling interest rate environment

8️⃣ Opt for Balance Transfer 💼

Similar to refinancing, but specifically to reduce EMI.

✔️ Benefits:

- Lower interest rate

- Reduced EMI

⚠️ Be careful:

- Transfer fees

- Terms & conditions

9️⃣ Increase Down Payment (Before Taking Loan) 🚗

If you haven’t taken the loan yet:

👉 Pay more upfront

Result:

- Lower loan amount

- Lower EMI

Simple but very effective.

🔟 Cut Unnecessary Loan Add-ons ❌

Sometimes lenders add:

- Insurance

- Processing charges

- Extra services

👉 These increase your loan burden.

Always review your loan breakdown.

Also Read : Basic Math Formulas Every Student Should Know 2026

🧡 Real-Life Example

Let’s make this real.

Rahul took a ₹8 lakh car loan at 10% interest for 7 years.

- EMI: ₹13,300

- He felt comfortable initially

After 1 year:

- His expenses increased

- EMI became stressful

What did he do?

✔️ Transferred loan to another bank at 8.5%

✔️ Made ₹1 lakh prepayment

Result:

- EMI reduced to ₹10,800

- Total interest also reduced

👉 Small smart moves = big financial relief

⚖️ Smart Strategy: Reduce EMI vs Reduce Interest

Here’s something important most people miss:

| Goal | Best Method |

|---|---|

| Lower EMI | Increase tenure |

| Save money overall | Reduce interest rate |

| Finish loan faster | Prepayment |

👉 Choose based on your priority.

🚫 Common Mistakes to Avoid

- ❌ Only focusing on EMI, ignoring total cost

- ❌ Not reading loan terms carefully

- ❌ Ignoring prepayment penalties

- ❌ Taking maximum tenure blindly

🧭 A Practical Rule You Can Follow

👉 Your EMI should not exceed 25–30% of your monthly income

If it does:

- Either reduce loan amount

- Or adjust tenure smartly

Frequently Asked Questions (FAQs) ❓

Can I reduce my EMI after taking a loan?

Yes 👍

You can:

Refinance

Prepay

Negotiate with lender

Is increasing tenure a good idea?

Only for temporary relief.

It reduces EMI but increases total interest.

Does prepayment always reduce EMI?

Not always.

You can choose:

Lower EMI

Or shorter tenure

Which is better: lower EMI or shorter loan?

Lower EMI = comfort

Shorter loan = savings

👉 Depends on your financial situation

Can banks reduce interest rate on request?

Sometimes yes—especially if:

You have a good repayment history

Market rates have dropped

Is balance transfer safe?

Yes, if done carefully.

Always compare total cost before switching.

🎯 Final Thoughts

Loans are not bad. They help us achieve important life goals.

But unmanaged EMIs can quietly become stressful.

The key is simple:

👉 Don’t just accept your EMI—optimize it.

A small effort like negotiating rates, prepaying a little, or choosing the right tenure can:

- Save you money 💰

- Reduce stress 😌

- Give you financial freedom faster 🚀

One Simple Reminder

“Your EMI should fit your life—not control it.”