💰 EMI vs Simple Interest: What’s the Difference?

When you take a loan or invest money, you’ll often hear two common terms:

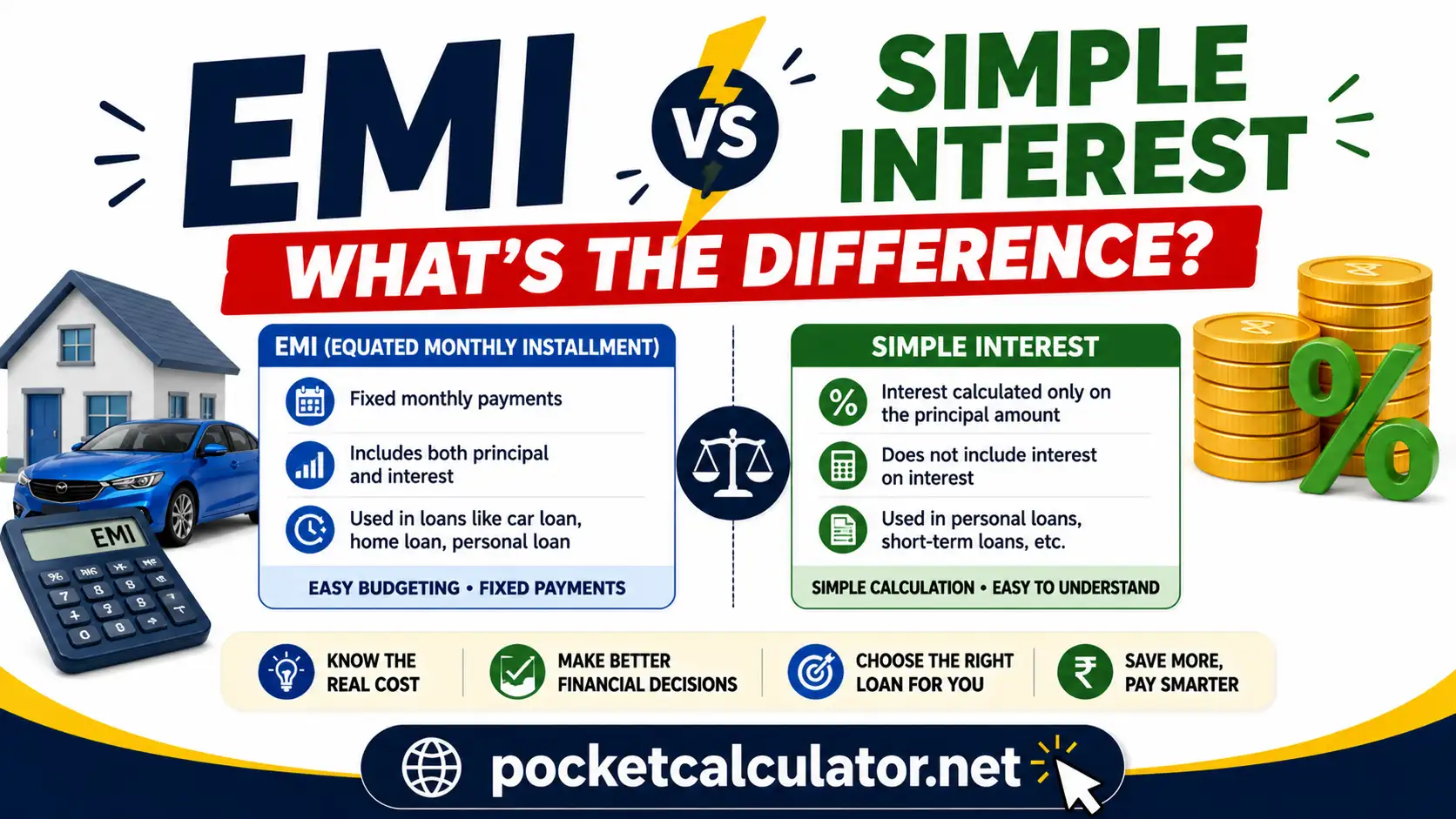

👉 EMI (Equated Monthly Installment)

👉 Simple Interest

At first glance, they might seem similar—they both involve borrowing and paying interest. But in reality, they work very differently.

If you don’t understand the difference, you could:

- Pay more than expected 💸

- Choose the wrong loan type 🤦♂️

- Struggle with repayments later

So let’s break this down in the simplest way possible—with examples, tables, and real-life clarity.

🤔 What is Simple Interest?

Simple Interest is the easiest form of interest calculation.

👉 You pay interest only on the original principal amount.

📌 Formula:

[

Simple Interest = \frac{P × R × T}{100}

]

Where:

- P = Principal (loan amount)

- R = Interest rate per year

- T = Time (in years)

🧮 Example of Simple Interest

Let’s say:

- Loan amount = ₹1,00,000

- Interest rate = 10% per year

- Time = 3 years

👉 Interest = (1,00,000 × 10 × 3) ÷ 100 = ₹30,000

👉 Total repayment = ₹1,30,000

💡 Key Feature

✔️ Interest remains constant every year

✔️ Calculation is simple and predictable

💳 What is EMI (Equated Monthly Installment)?

EMI is how most modern loans are repaid.

👉 Instead of paying everything at once, you repay in monthly installments.

Each EMI includes:

- 💰 Principal repayment

- 📈 Interest (on remaining balance)

🔍 Important Difference

Unlike simple interest:

👉 EMI interest is calculated on the reducing balance, not the original amount.

This means:

- Early EMIs = more interest

- Later EMIs = more principal

📊 EMI Calculation (Basic Idea)

The formula exists—but let’s not overcomplicate it.

👉 EMI depends on:

- Loan amount

- Interest rate

- Tenure

Example:

- Loan = ₹1,00,000

- Rate = 10%

- Tenure = 3 years

👉 EMI ≈ ₹3,226 per month

Total paid ≈ ₹1,16,000

Also Read : How to Reduce EMI on Your Loan 2026 (Smart Tips That Actually Work)

⚖️ EMI vs Simple Interest: Side-by-Side Comparison

Here’s where things get really clear:

| Feature | EMI (Reducing Balance) | Simple Interest |

|---|---|---|

| Interest Calculation | On remaining balance | On original amount |

| Payment Method | Monthly installments | Usually lump sum |

| Interest Cost | Lower overall | Higher (if long-term) |

| Complexity | Moderate | Very simple |

| Common Usage | Home, car, personal loans | Short-term loans, informal lending |

🧠 The Real Difference (In Simple Words)

👉 Simple Interest = Flat calculation

👉 EMI = Dynamic calculation

Think of it like this:

- Simple interest doesn’t “care” that you’re repaying gradually

- EMI adjusts interest as your loan reduces

🧮 Real-Life Comparison Example

Let’s compare both for the same loan:

- Amount: ₹2,00,000

- Rate: 10%

- Time: 2 years

📌 Simple Interest

- Interest = ₹40,000

- Total = ₹2,40,000

📌 EMI Method

- EMI ≈ ₹9,230/month

- Total paid ≈ ₹2,21,500

🔥 Result:

👉 EMI saves you around ₹18,500

That’s a big difference for the same loan.

🧡 A Real-Life Story (Human Touch)

Ankit needed ₹1.5 lakh urgently.

He had two options:

1️⃣ Borrow from a local lender at simple interest

2️⃣ Take a bank loan with EMI

The local lender said:

👉 “Only 12% simple interest, no paperwork.”

Sounded easy.

But after 2 years:

- He paid much more than expected

- Interest didn’t reduce even after partial payments

Meanwhile, his friend chose EMI:

- Paid monthly

- Interest reduced over time

👉 In the end, Ankit realized:

“Simple doesn’t always mean cheaper.”

⚠️ Common Misunderstandings

❌ “Simple Interest is always better”

Not true. It’s simpler—but often more expensive.

❌ “EMI is complicated, so avoid it”

Modern tools make EMI easy—and usually more cost-effective.

❌ “Monthly payment means more interest”

Actually, EMI reduces interest over time due to reducing balance.

🧭 When Should You Choose What?

👉 Choose EMI if:

- You want structured monthly payments

- You prefer lower total interest

- You’re taking a long-term loan

👉 Choose Simple Interest if:

- Loan is very short-term

- You want easy calculation

- It’s a small amount

📊 Visual Insight Table

| Scenario | Better Option |

|---|---|

| Home Loan (20 years) | EMI |

| Car Loan (5 years) | EMI |

| Short-term borrowing (3–6 months) | Simple Interest |

| Informal borrowing | Simple Interest |

💡 Smart Tips Before Choosing

- ✔️ Always calculate total repayment

- ✔️ Don’t get fooled by “low monthly burden”

- ✔️ Ask lender how interest is calculated

- ✔️ Compare both methods before deciding

Frequently Asked Questions (FAQs) ❓

Which is cheaper: EMI or Simple Interest?

👉 Usually EMI, because interest is calculated on reducing balance.

Why does EMI feel easier to manage?

Because payments are spread monthly, making budgeting easier.

Can EMI loans have higher interest rates?

Yes, but still may cost less overall due to reducing balance calculation.

Is simple interest used by banks?

Rarely for long-term loans. Banks mostly use EMI-based systems.

Can I convert simple interest loan to EMI?

Not usually. It depends on lender policies.

Which is better for beginners?

👉 EMI, because it’s structured and widely used.

🎯 Final Thoughts

Understanding EMI vs Simple Interest is not just about math—it’s about making smarter financial decisions.

Here’s the simplest takeaway:

👉 Simple Interest is easy to calculate

👉 EMI is smarter for long-term savings

Before taking any loan, don’t just ask:

❌ “What’s the monthly payment?”

Instead ask:

✅ “How is the interest calculated?”

Because that one question can save you thousands.

One Line to Remember

“Simple interest looks easy, but EMI often saves money.”