When people talk about EMI, they usually focus on just the monthly number. But that number is the result of a few powerful factors working behind the scenes. If you understand these, you stop guessing—and start controlling your loan decisions.

Let’s break down the two biggest drivers of your EMI in the simplest possible way.

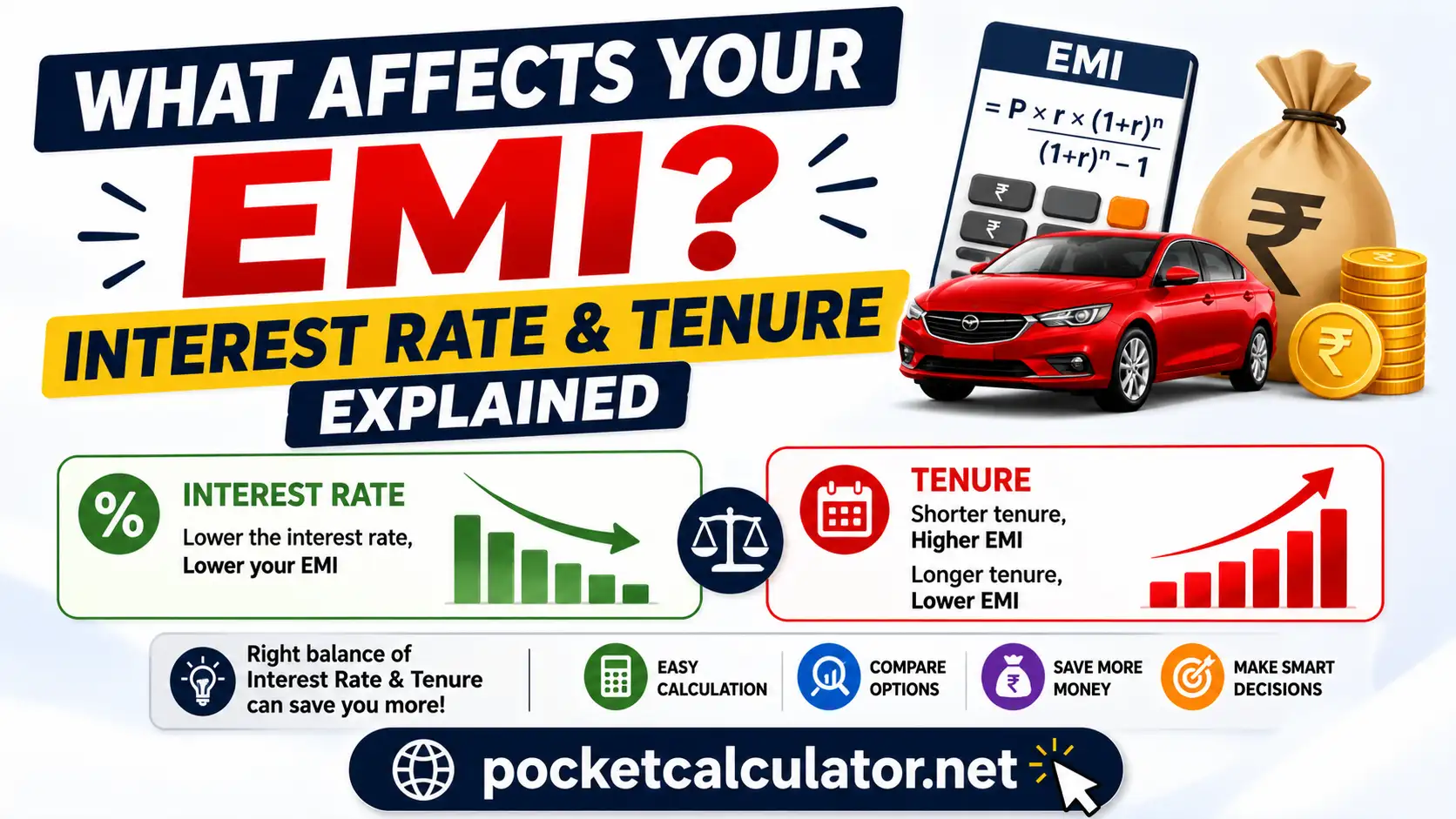

💡 What Affects Your EMI? Interest Rate & Tenure Explained

At its core, your EMI depends mainly on:

- 📈 Interest Rate

- ⏳ Loan Tenure

(Loan amount matters too, but today we’ll focus on the two factors that people often misunderstand.)

📈 1. Interest Rate: The Silent Cost Multiplier

The interest rate is what the lender charges you for borrowing money. Even a small difference here can have a surprisingly big impact.

🔍 How It Affects EMI

- Higher interest rate → Higher EMI

- Lower interest rate → Lower EMI

But here’s the catch:

👉 It doesn’t just affect your EMI—it affects the total amount you repay over time.

🧮 Simple Example

Let’s say you take a ₹5,00,000 car loan for 5 years:

| Interest Rate | EMI (approx) | Total Interest Paid |

|---|---|---|

| 8% | ₹10,140 | ₹1,08,000 |

| 10% | ₹10,620 | ₹1,37,000 |

👉 Just a 2% increase in interest:

- EMI increases slightly

- But total interest increases by ₹29,000

That’s the real impact.

🧠 What Decides Your Interest Rate?

- ✔️ Your credit score

- ✔️ Your income stability

- ✔️ Loan type (fixed vs floating)

- ✔️ Bank/NBFC policies

👉 If your credit score is strong, you have real negotiating power.

⏳ 2. Loan Tenure: The Balancing Act

Loan tenure is simply how long you take to repay the loan.

This is where most people make emotional decisions—choosing lower EMI without thinking long-term.

🔍 How It Affects EMI

- Longer tenure → Lower EMI

- Shorter tenure → Higher EMI

Sounds good, right? Lower EMI feels easier.

But here’s the reality 👇

🧮 Example Comparison

Loan: ₹5,00,000 at 9% interest

| Tenure | EMI (approx) | Total Interest Paid |

|---|---|---|

| 3 years | ₹15,900 | ₹72,000 |

| 5 years | ₹10,400 | ₹1,24,000 |

| 7 years | ₹8,000 | ₹1,72,000 |

⚖️ What This Really Means

- ⏳ Longer tenure saves you monthly cash flow

- 💸 But you pay much more interest overall

👉 In this example:

- Choosing 7 years over 3 years costs you ₹1 lakh extra

That’s the trade-off people often ignore.

🤝 Interest Rate vs Tenure: How They Work Together

Think of it like this:

- Interest rate decides how expensive your loan is

- Tenure decides how long you stay in debt

Together, they shape:

👉 Your EMI

👉 Your total repayment

👉 Your financial comfort

🧠 A Practical Way to Decide

Here’s a simple approach that actually works in real life:

Step 1: Fix a Comfortable EMI

- Ideally 20–25% of your monthly income

Step 2: Adjust Tenure Accordingly

- If EMI is too high → increase tenure slightly

- If manageable → reduce tenure to save interest

Step 3: Always Compare Interest Rates

- Even 0.5% difference matters over time

🧡 Real-Life Scenario

Priya and Amit both took a ₹6 lakh car loan.

- Priya chose 7 years for lower EMI

- Amit chose 5 years with slightly higher EMI

After repayment:

- Priya paid ~₹2 lakh interest

- Amit paid ~₹1.4 lakh interest

👉 Amit saved ₹60,000 just by choosing a shorter tenure.

Same car. Same loan. Different thinking.

Also Read : Input Tax Credit (ITC) Explained Simply

⚠️ Common Misunderstandings

❌ “Lower EMI is always better”

Not true. Lower EMI often means higher total cost.

❌ “Interest rate difference is small, doesn’t matter”

Even a 1% difference can cost you thousands or lakhs.

❌ “Long tenure gives flexibility”

It does—but at a price you may not notice immediately.

🎯 Smart Tips to Optimize Your EMI

- ✔️ Improve your credit score before applying

- ✔️ Compare at least 3 lenders

- ✔️ Don’t blindly choose maximum tenure

- ✔️ Prepay when you have extra cash

- ✔️ Negotiate interest rates (many people don’t!)

FAQs ❓

Which affects EMI more: interest rate or tenure?

Both matter, but:

Interest rate affects total cost

Tenure affects monthly affordability

Can I change tenure later?

Sometimes yes, through refinancing or restructuring—but terms vary by lender.

Is shorter tenure always better?

Financially yes (less interest), but only if EMI stays comfortable.

How can I get the lowest interest rate?

Maintain good credit score

Show stable income

Compare banks before finalizing

What’s the biggest mistake to avoid?

Choosing EMI based only on what “feels affordable” without checking total repayment.