Buying a home is one of the biggest financial decisions you’ll ever make. For most people, it’s not possible to pay the entire amount upfront—so they rely on a home loan. And that’s where EMI (Equated Monthly Installment) becomes a crucial part of your life. (Home Loan EMI)

But let’s be honest—EMI calculations can feel confusing at first. 🤯

Don’t worry. By the end of this article, you’ll clearly understand how home loan EMI works, how to calculate it step by step, and how to make smarter financial decisions.

💡 What is EMI?

EMI (Equated Monthly Installment) is the fixed amount you pay every month to repay your home loan. It includes:

- Principal Amount (the money you borrowed)

- Interest Amount (the cost of borrowing)

Every month, a portion of your EMI goes toward interest, and the rest reduces your principal.

📊 Why Understanding EMI is Important

Understanding EMI isn’t just about math—it’s about control.

- Helps you plan your budget

- Prevents over-borrowing

- Lets you compare different loan offers

- Helps you choose the right loan tenure

In simple words: EMI knowledge = smarter financial decisions 💰

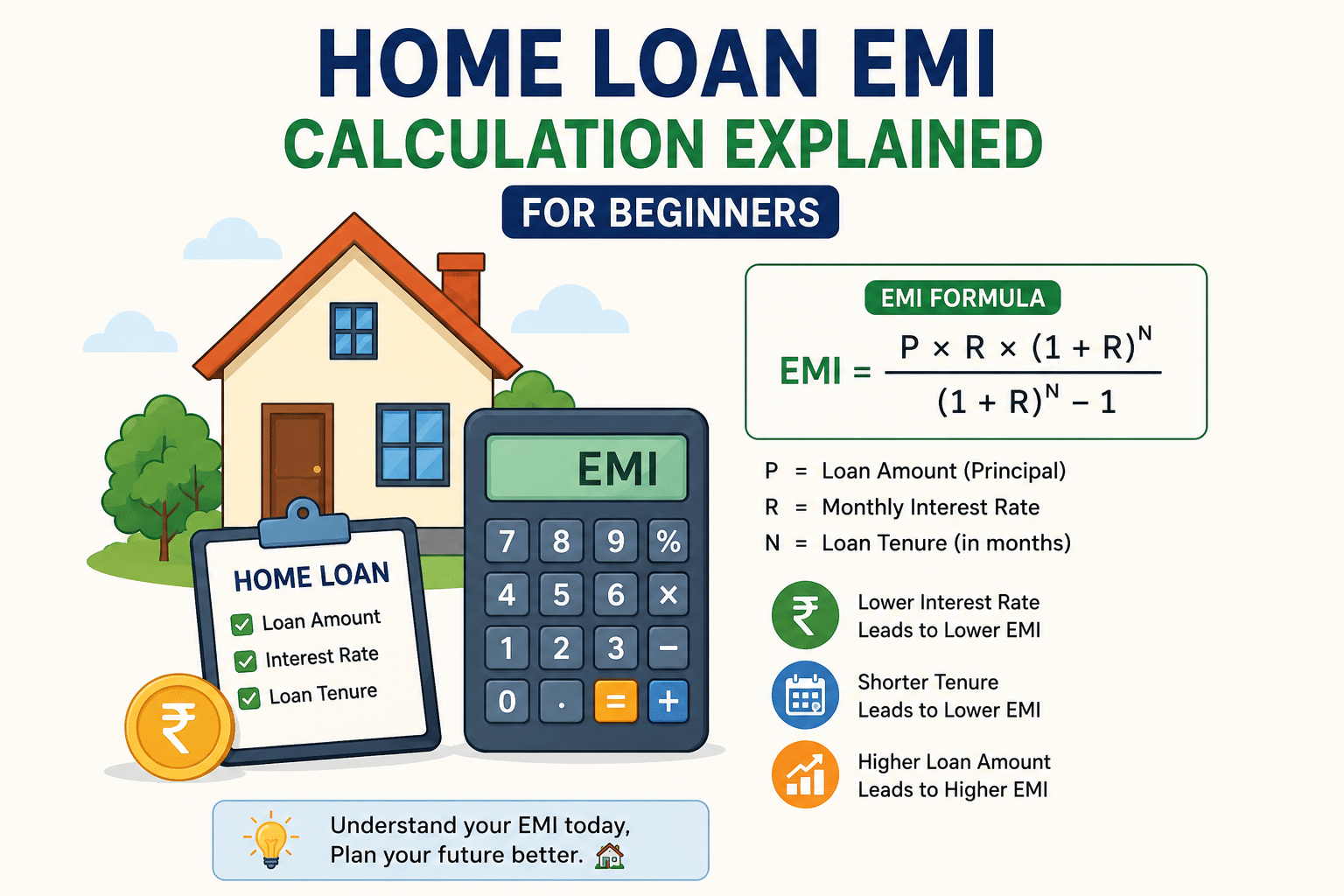

🧮 Home Loan EMI Formula

Here’s the standard formula used to calculate EMI:EMI=(1+R)N−1P×R×(1+R)N

Where:

- P = Loan Amount (Principal)

- R = Monthly Interest Rate (Annual rate ÷ 12 ÷ 100)

- N = Loan Tenure (in months)

🔍 Step-by-Step EMI Calculation

Let’s break it down into simple steps.

Step 1: Know Your Loan Details

Assume:

- Loan Amount = ₹30,00,000

- Interest Rate = 8% per year

- Loan Tenure = 20 years

Step 2: Convert Interest Rate to Monthly

R=12×1008=0.00667

Step 3: Convert Tenure into Months

N=20×12=240

Step 4: Apply the Formula

After calculation:

👉 EMI ≈ ₹25,093 per month

📘 Real-Life Example (Simple & Relatable)

Let’s say Rahul wants to buy his dream home. 🏠

- Property Cost: ₹40 lakh

- Down Payment: ₹10 lakh

- Loan Amount: ₹30 lakh

- Interest Rate: 8%

- Tenure: 20 years

Rahul’s EMI comes out to around ₹25,000/month.

Now here’s the important part:

👉 Over 20 years, Rahul will pay:

- Total EMI Paid = ₹25,093 × 240 = ₹60,22,320

- Interest Paid = ₹30,22,320 😲

That’s more than the loan amount itself!

This is why understanding EMI matters—it shows the true cost of your loan.

Also Read : How to Calculate Time Difference Between Two Dates in 2026

📊 EMI Breakdown Table

| Year | EMI Paid (Yearly) | Principal Paid | Interest Paid | Remaining Balance |

|---|---|---|---|---|

| 1 | ₹3,01,116 | ₹55,000 | ₹2,46,116 | ₹29,45,000 |

| 5 | ₹3,01,116 | ₹75,000 | ₹2,26,116 | ₹27,00,000 |

| 10 | ₹3,01,116 | ₹1,20,000 | ₹1,81,116 | ₹21,00,000 |

| 15 | ₹3,01,116 | ₹2,00,000 | ₹1,01,116 | ₹12,00,000 |

| 20 | ₹3,01,116 | ₹3,00,000 | ₹1,116 | ₹0 |

👉 Notice how interest is higher in early years and reduces over time.

⚖️ Factors That Affect Your EMI

1. Loan Amount 💰

Higher loan = higher EMI

2. Interest Rate 📈

Even a small increase can significantly raise EMI

3. Loan Tenure ⏳

- Longer tenure = lower EMI but more interest

- Shorter tenure = higher EMI but less interest

🔄 Fixed vs Floating Interest Rate

Fixed Rate 🔒

- EMI stays constant

- Safe but slightly higher interest

Floating Rate 🌊

- EMI changes with market rates

- Can be cheaper—but riskier

📱 Easy Ways to Calculate EMI

You don’t always need to do manual calculations.

1. Online EMI Calculators

Quick and accurate

2. Excel Formula

Use:

=PMT(rate, nper, pv)3. Mobile Apps

Many banking apps provide EMI calculators

💡 Tips to Reduce Your EMI Burden

✅ Make a Higher Down Payment

Lower loan = lower EMI

✅ Choose Shorter Tenure (if affordable)

Saves huge interest

✅ Prepay Your Loan

Even small extra payments reduce interest significantly

✅ Compare Lenders

Even 0.5% difference matters

⚠️ Common Mistakes to Avoid

❌ Ignoring total interest paid

❌ Choosing long tenure just for low EMI

❌ Not reading loan terms carefully

❌ Borrowing beyond your capacity

❤️ A Human Perspective

A home loan isn’t just numbers—it’s your future.

It’s about:

- Your family’s comfort

- Your financial stability

- Your peace of mind

An EMI that looks “manageable” today shouldn’t become stressful tomorrow.

Take your time. Understand the math. Plan wisely.

Follow : PocketCalculator.net

What is a good EMI amount for my salary?

A safe rule: EMI should not exceed 30–40% of your monthly income.

Can I change my EMI later?

Yes, through:

Loan restructuring

Prepayment

Balance transfer

What happens if I miss an EMI?

You may face:

Penalty charges

Credit score damage

Is prepayment always beneficial?

Mostly yes 👍

It reduces interest—but check for prepayment charges.

Which is better: long tenure or short tenure?

Short tenure = less interest

Long tenure = lower EMI

Choose based on your financial comfort.

How much home loan can I afford?

Depends on:

Your income

Existing debts

Lifestyle expenses

Home Loan EMI Calculation Online | Home Loan EMI Calculation Trick | Home Loan EMI Calculation Guide | Home Loan EMI Calculation